Introduction Unified Pension Scheme (UPS) is Master pension reform announced by Government of India with endeavour to provide financial security, guaranteed minimum pension and retiring post life dignity to the employees of central government. The scheme is intended as a bridge between the Old Pension Scheme (OPS) and the National Pension System (NPS), providing a fair amount of pension coupled with contributory coverage.

With rising feelings of apprehension amongst Government employees about the uncertainty associated with NPS, UPS has delivered a balanced as well as forward looking option. This article describes everything that’s there to know about NPS like what is UPS, who all are eligible for starting one, and the benefits of having a UPS alongside with contribution structure of such pension and other!!

WHAT IS THE UNIFIED PENSION SCHEME (UPS) ?

The Union Pension Scheme (UPS) is a government supported pension which offers monthly pension till death with family pension, inflation protection and the payout of the balance in case of exit from the scheme before purchasing annuity.

In NPS, unlike Universal Pension Scheme (UPS) which provides for a minimum guaranteed pension and creates much needed social security for the elderly, pensions are subservient to market performance.

For eligible central government employees, UPS is effective from April 1, 2025.

Rational Behind Introduction of Unified Pension Scheme

The UPS came in as the following dissatisfaction for market linked NPS model rose. Employees demanded:

- Pension entitlement like the Old Pension Scheme

- Protection against market volatility

- Inflation-adjusted retirement income

- Family members’ security after death

UPS was created by government to:

- Pension certainty

- Fiscal sustainability

- Long-term social security

Unified Pension Scheme Eligibility Criteria

Who Can Opt for UPS?

Under the UPS Unified Pension Scheme, eligible categories include:

1.Existing Central Government Employees

- As on 1st April, 2025, the employees under NPS.

2.New Government Recruits

- Employees appointed on after 1 april,2025

3.Retired NPS Subscribers

- Some retirees who retired before 31 March 2025 (in limited circumstances)

Who Is Not Eligible?

- Dismissed or discharged employees

- Staff having less than 10 years of qualifying service

UPS Contribution Structure (Employee & Government)

| Contributor | Contribution Rate |

| Employee | 10% of Basic Pay + DA |

| Government | 18.5% of Basic Pay + DA |

How Government Contribution is Used

- 10% goes to the individual pension account

- 8.5% goes to a common pooled fund to support guaranteed pensions

This higher government contribution makes UPS financially stronger than NPS.

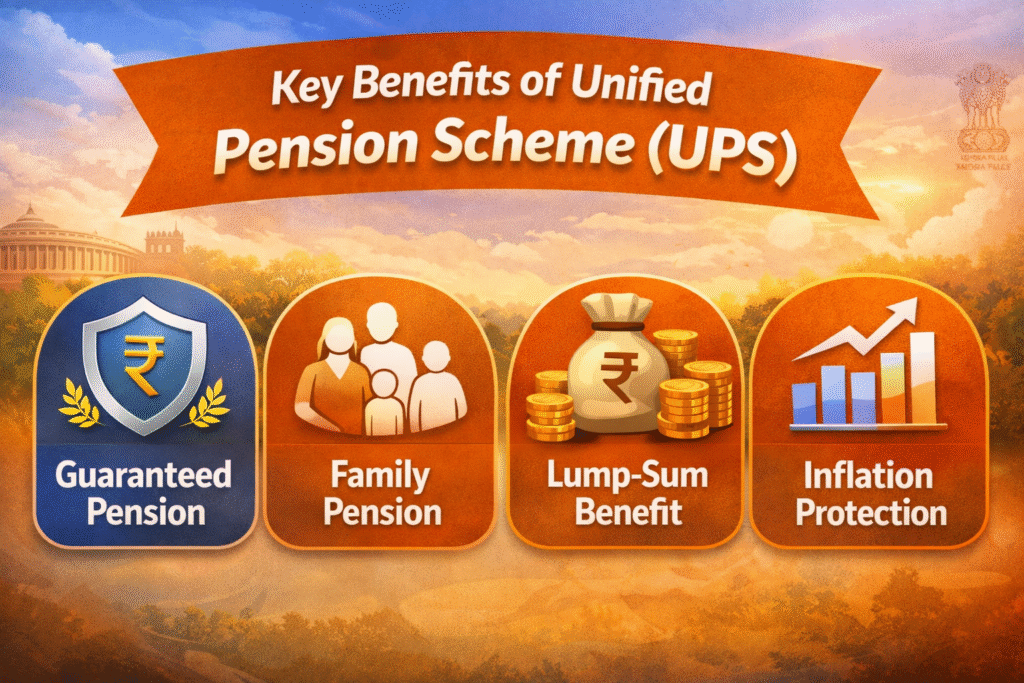

Unified Pension Scheme Benefits

1.Assured Monthly Pension

Employees with 25 or more years of allowable service earn:

50% of average basic pay of the preceding 12 months at date of retirement

OSSIt The claims measure operates, then, to make UPS like OPS in terms of pension certainty.

2.Minimum Guaranteed Pension

Workers with jobs for 10 to 25 years receive a minimum pension of ₹10,000 p/m

Pension is proportionate for service of 10-25 years

This will have to provide the means for dignity and financial security for shorter service even.

3.Family Pension Under UPS

In the event of death of the pensioner:

- The wife is entitled to 60% of the final pension paid out

- Dearness Relief (DR) is applicable

This, in turn, makes UPS a family safe pension scheme and unlike NPS where the annuity terms change.

4.Dearness Relief (Inflation Protection)

Dearness Relief (DR) is applied on the UPS pensions for inflation.

✔ Linked to AICPI-IW (All India Consumer Price Index-Industrial workers)

✔ Insulates retirees from inflationary pressures on cost of living

5.Lump-Sum Payment on Retirement

Upon retirement on superannuation, an employee is entitled to:

1/10th of last drawn (Basic + DA) for each completed 6 monthly period.

🔹 This does not include the tip

🔹 Doesn’t lower monthly pension

Also read this: PM Gati Shakti Yojana

UPS Withdrawal & Exit Rules

- At least 40% and maximum up to 60% of the pension wealth which has been accumulated until retirement date, can remain invested.

- Increased withdrawal =reduced assured pension

- Withdrawals in part may be permitted in certain circumstances

UPS wants its workers to depend on pensions, not lump sums.

Unified Pension Scheme vs NPS (Comparison Table)

| Feature | UPS | NPS |

| Pension Guarantee | Yes | No |

| Minimum Pension | ₹10,000 | Not Guaranteed |

| Inflation Protection | Yes | Limited |

| Family Pension | Assured | Depends on annuity |

| Government Contribution | 18.5% | 14% |

| Market Risk | Low | High |

Conclusion

UPS is ideal for employees seeking security and predictability, while NPS suits those willing to take market risks.

UPS Opt-In Process & Deadline

- Current NPS staff will have to choose for UPS within stipulated time frame

- Non-opt out = continuity under NPS

- Choice is generally irrevocable

Employees should consider long-term benefits before choosing.

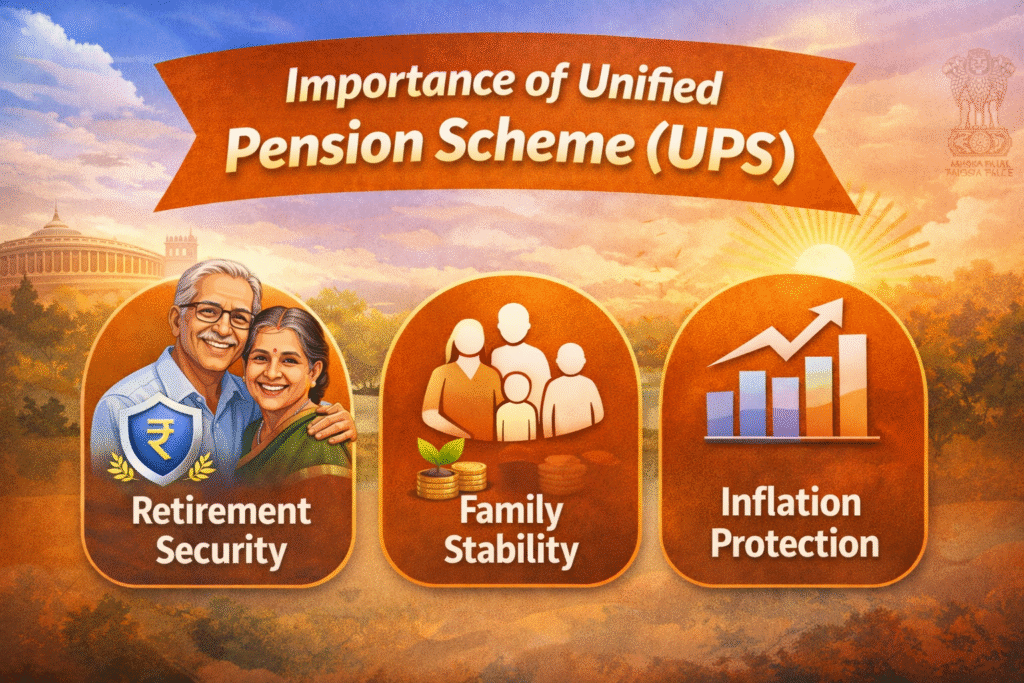

Importance of Unified Pension Scheme

1.Retirement Security

UPS provides reliable, pension income in retirement and minimizes the reliance on savings.

2.Social Welfare

Social Protection Family pension and inflation indexing add to social protection.

3.Economic Stability

Managing the balance of workers’ welfare and fiscal prudence.

Future Scope of UPS in India

- Possible adoption by state governments

- Could impact policy on public sector pensions

- Could end up as national model of pension security

UPS is being closely tracked as a replacement-readily available alternative to OPS.

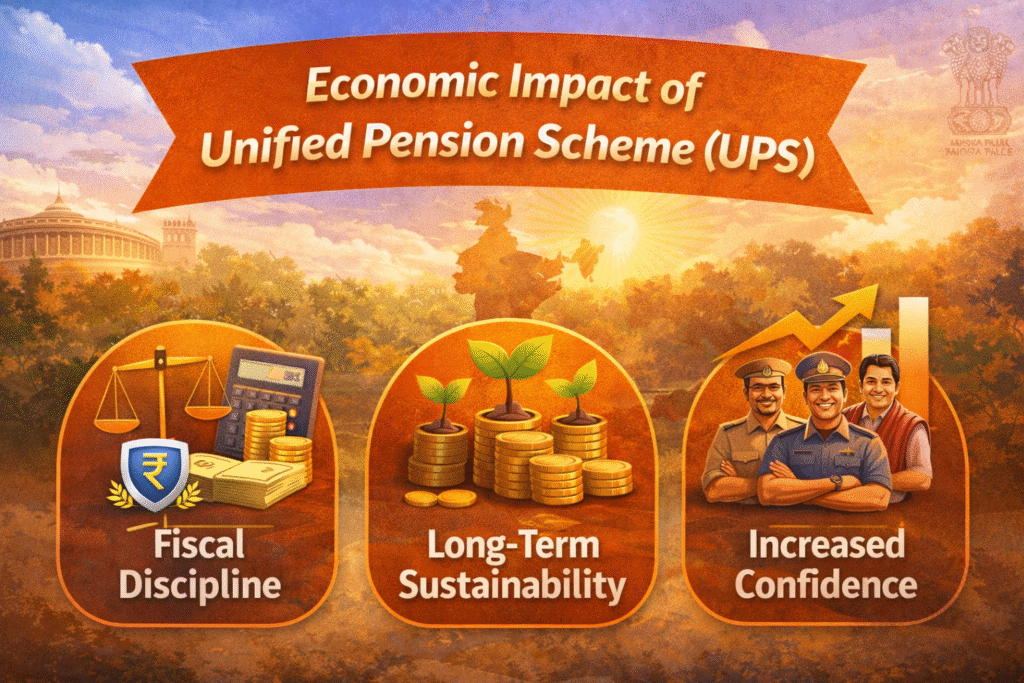

Economic Impact of Unified Pension Scheme on India

1. Fiscal Discipline

UPS avoids the heavy pension burden associated with OPS.

2. Long-Term Sustainability

The pooled fund model ensures pension payouts remain stable.

3. Increased Employee Confidence

Secure retirement boosts morale and productivity.

This makes UPS a policy-balanced pension reform.

Conclusion

The Unified Pension Scheme (UPS) is an historic step for secure, stable and inflation-protected pension for the Central government employees. Providing the security of pension to families and ensuring higher government contribution, UPS addresses the NPS limitation while being fiscally disciplined.

Employees will benefit from an India designed “future pension solution” that would ensure long-term retirement security when they retire.

Also read this: Nijut Moina 2025 Scheme | Ladkibahin Maharashtra Gov in ekyc | Gaon Ki Beti Yojana

FAQs

Q1. Is the Unified Pension Scheme better than NPS?

Yes, UPS is better for employees seeking assured pension and lower risk, while NPS is market-linked.

Q2. What is the minimum pension under UPS?

The minimum guaranteed pension under UPS is ₹10,000 per month.

Q3. Is UPS applicable to state government employees?

Currently, UPS applies to central government employees only.

Q4. Can I switch from NPS to UPS?

Yes, eligible employees can opt for UPS within the notified window.

Q5. Is UPS the same as the Old Pension Scheme?

No, but UPS combines OPS-like pension security with contributory funding.